This week: “I am a 27-year-old psychology teaching associate at a university while completing my PhD.

Education has always been something that I’ve loved. My degree was paid for with student loans which I am now paying back. I won a scholarship for my PGCE, so that was all paid for. I also won a fully funded scholarship for my PhD so again, that is all pretty much paid for now. I feel extremely fortunate to be in this position.

My family have always been extremely open about every topic you can think of. Along these lines, finances were also openly discussed. As a result, I have always felt rather clued up about my dollar. Having these types of discussions with my parents makes my life a whole lot easier.

The plan is that my parents will move in with A (my boyfriend) and I, once we have bought a house. This is also the expectation with his mum and partner. A and I feel very strongly that you should look after your own (although we completely understand that this is not always possible) and while it is feasible we would much rather care for our parents under our own roof. When this occurs, the plan is that our share of inheritance money will be invested into our home.”

Occupation: Psychology teaching associate/PhD student

Industry: Higher education

Age: 27

Location: London

Salary: £22,000 for teaching associate/£16,500 for PhD stipend

Paycheque amount: (TA paycheque is monthly. Stipend is quarterly): £1,500

Number of housemates: Two. My partner, A, and also A’s mum’s partner, R.

Monthly Expenses

Housing costs: I pay A’s mum £300 per month (which, considering we are basically in central London, is beyond a bargain). This includes all bills, so we don’t pay any extra on top of that.

Loan payments: Student loan payment. £200 to my credit card.

Savings? I have a Monzo account, which I transfer my disposable income and savings into. I currently have five Monzo pots: £111 in an Easy Access Savings Pot (I have the option where I round up spending on my current account and the pennies go in here); £565 in a Holidays Pot; £240 in an Emergencies Pot; £200 in a Christmas Presents Pot; £1,460 in a Chanel Handbag Pot (this will be my “Well done for completing your PhD” present from me to me, love me). I also have £600 in a Help to Buy ISA and £3 in my Santander ISA (lol). I also currently have £500 set aside to go into a Premium Bond, I am just waiting for it to be set up and then I will transfer the money over. A and I just pay for stuff and then split the bill via our Monzo accounts, which works really well.

All other monthly expenses: £15 p/m for my phone, which gives me unlimited calls, data, etc – I bought it outright about four years ago and it is still in perfect nick. £200 p/m for travel, which makes me feel sick, but at least I am saving on rent. £40 p/m for personal health – this consists of medication payments. £14.99 p/m Spotify Family account – my dad transfers £7.50 to me each month to share this. £8.99 p/m Netflix account – my brother and his partner, her two children and their twins (age 2) all leech off my account. Although I do rinse his Disney+ for free, so swings and roundabouts. Charity donations include £5 p/m to Whitechapel Mission and £5 p/m to The Children’s Society. I plan to set up a monthly payment out of my paycheque to go to charities, your employer then matches your donation (a bit like Gift Aid).

8.30am: Morning has broken and as a faithful follower of Craig David, I shall chill on Sunday. I’m currently reading Nigel Slater’s Toast and I am absolutely loving it! I snuggle in bed with a coffee and continue reading. A interrupts my reading with a video he’s found on Reddit. It’s a montage of different Disney Princess videos to “WAP” and it’s up there with one of the most disturbing things I have ever seen. And also equally hilarious. We forward it to our equally disturbed friend, N, and exchange many laughing emoji.

9.30am: A starts prepping a chilli for the slow cooker while I FaceTime my dad. Today is his 70th birthday, so I sing “Happy Birthday” while performing a dance routine; talent. He loves it and we go on to discuss all his presents. Next weekend, A and I will be treating him and Mum to lunch at a posh restaurant near them. Dad doesn’t know this yet so I smugly remind him that his birthday celebrations shall continue next weekend… *vanishes in puff of smoke*

9.45am: Absolute disaster. We’ve run out of eggs which is a massive issue for breakfast. Instead we have a slice of breakfast quiche each. If you love a savoury breakfast but cba to get up and cook in the mornings, I present to you: The Breakfast Quiche. It consists of puff pastry, goat’s cheese, spinach and mushrooms, baked in the oven and voilà. You’re welcome.

10am: We have some decorators coming in this week to patch up the aftermath of the shoddy workmanship of some absolutely bastard roofers. I could honestly write an entire essay about this but I shall spare you. In prep, we have to move all of our furniture and it’s effort. Craig David would be displeased.

11am: Showered, teeth brushed and morning skincare routine complete (CeraVe foaming cleanser; The Ordinary hyaluronic acid; CeraVe non-perfumed dry touch gel-cream; The Ordinary caffeine solution). Put on some activewear. A and I decide to go out for a long walk today, so we get prepped and head out.

1pm: Had such a lovely long walk. We also got coffees en route – A pays on his Monzo and then splits with me. I pay £2.20 for a dirty chai latte. We pass Tesco on our way back and pop in to get beers for A, ciders for me, two tubes of Pringles and micellar water. I pay £12.45 for my share and the micellar water. When we get home A makes us cheese and ham toasties (honestly, so delish) while we watch MasterChef: The Professionals. I suggest A enters and cooks different toasties each round and then a deconstructed toastie for the final. Marcus would love it.

2pm: A plays video games while I prep a smoothie for tomorrow: apples, honey, cinnamon, vanilla extract, porridge oats and cashew milk. I then clean the bathroom while listening to the Up and Vanished podcast. After this, I snuggle down next to A and continue reading Toast.

4pm: A colleague recently received a promotion so A and I order her some flowers online: £15.75, A transfers me his half, so I pay £7.88. We’ve also been discussing signing up for an Oddbox (inspired by a previous Money Diary). We have a gander and decide on the small veg box to start us off. £10.99 but this won’t come out until our first box arrives in a couple of weeks.

7pm: After a few hours of A playing video games and me finishing off Toast (rather impressed with myself considering I started it only last night), it’s time for dins. I have leftover tofu pad Thai with spring rolls, A has leftover beef bourguignon. Of course, we accompany this with MasterChef: The Professionals.

9pm: Teeth brushed and evening skincare routine complete (CeraVe foaming cleanser; The Ordinary toner; The Ordinary retinol) and then snuggle in bed with A while watching Dark on Netflix. Watching this literally makes me feel like the brain exploding GIF with the fireworks in the background.

10.30pm: ‘Tis bedtime. I put on my Bluetooth sleep mask (a game-changer if you struggle to get to sleep/have nighttime anxiety – hi) and listen to Shadowed by Death by Maurice LeBlanc on The Classic Tales Podcast.

Total: £22.53

7am: Ugh.

7.25am: Listen to our morning routine on Alexa. Apparently, Mariah Carey is going to be doing thoughts for the day over the course of this week. A groans in despair.

7.25am: Normally, we would get up and go for a morning walk now but we need to finish moving furniture for these decorators. I slither out of bed like a slug and slide into the shower.

7.45am: Decide against a shower as I actually fancy a bath later. Tomorrow will be my first day back in the office since March *screams* so I plan on a spa evening tonight to get prepped. I brush my teeth and do my morning skincare routine with the addition of my rose quartz facial roller, get dressed and head downstairs while A blares “Jesus Walks” by Kanye West and I rap (most of) the lyrics.

8am: No breakfast quiche left and our groceries don’t arrive until Wednesday (cry, cry, cry, cry, cry, cry) so I have some salted caramel spread on toast to compensate. I wash this down with an Actimel, orange juice, some feroglobin water (great for added energy) and my breakfast smoothie. I read a Money Diary while I do this (so meta, so wow).

8.45am: Check my personal emails and see that my Kapten & Son backpack I ordered last week is arriving today – yes! I literally buy ALL my clothes secondhand off Depop, so spending £100 on a backpack was a big deal for me. However it’s gorgeous and great quality and shall be worn to death as my old Kanken was, RIP.

12pm: Remarkably, I have been fairly productive this morning. I’ve read up on the topics I am teaching this week and have also worked on some paper edits. I recently received a rejection from a journal (cry, cry) but the feedback is really useful and is actually helping me to strengthen the paper. So initially boo but now yay.

12.15pm: Cheese and jam sandwich for lunch (trust me), a packet of Squares and a Curly Wurly, because I am 10 years old. Gobble this down while watching Below Deck on HayU.

3pm: Down a coffee in record time before entering a teaching meeting. Luckily, I am teaching with my bestie, C, on this module, so the meeting is actually a good laugh.

4pm: Happy with my afternoon – again, nice and productive! Feeling really happy with how my paper is taking shape. High five, science! A and I decide to go for a walk.

6.15pm: Back from a lovely long walk. We got some takeaway ciders from a pub opposite en route. A pays and my share is £4, of course I get a Rekorderlig like the basic bitch I am. We prep dinner as soon as we get in; we’re having A’s slow-cooked chilli (it’s been cooking for over 24 hours – yummy!). A has his with rice, I have mine with spaghetti and we continue watching Below Deck as we eat.

7pm: Prep lunch for tomorrow: ham and mayo sandwich, packet of Quavers and Curly Wurly (remember, I’m 10) and pop it in my new biodegradable bamboo lunchbox (exciting!). Also get my backpack packed and ready. After this, I run my bath. When it comes to baths, I do not fuck about. I run a hot bath with lavender and honey bath salts, gingerbread bath salts and Dead Sea salts, with the addition of my rainbow glitter bath pillow (so bougie). I soak while listening to the Up and Vanished podcast.

8pm: I do some parkour to get to my PJs – everything is all over the place in our bedroom because of the decorators. Once I am ready for bed, I snuggle down with A. We watch The Meg, which is astonishingly shite. Considering Jason Statham plays the exact same role in every film, it’s impressive how diabolical his acting is in this. We keep cracking up about this and decide we should name our firstborn The Meg. No surname, just The Meg.

9pm: Brush teeth and do evening skincare routine (swap out the retinol for The Ordinary azelaic acid this time). Put on my sleep mask and continue listening to The Classic Tales Podcast. P.S. I don’t want to wake up at 6am help meeeeeeeeeeeeeeee.

Total: £4

5.45am: Help me.

6am: Alexa tells me it’s 15 degrees but it’s dark and rainy so for reasons I later regret I do not take heed of this information.

6.50am: Showered, morning skincare routine complete, brush teeth, brush hair, do minimal makeup (but add eyeliner flick because ooh, first day back), get dressed, make coffee for travel mug, grab backpack, “A, can you get my coat? I can’t reach it”, kiss A, oh no I need my face shield, grab face shield, bolt out of door and BREATHE.

7.20am: Omg I totally underestimated how warm it would be. I. Am. Sweating. I literally stood on the Tube dripping beads of sweat. I look like I am going through the menopause. I get on the Overground and literally strip. Try to restore balance, drink my feroglobin water and listen to an audiobook of The Adventures of Huckleberry Finn by Mark Twain. I’ve started the Gilmore Girls reading challenge: you have to read all 339 books mentioned by Rory Gilmore across the series. £17.20

9.30am: I spilled coffee down my blouse and dropped all the cards out of my purse on the platform. Wicked. Other than that, I am in my office and all is well. I pop to the campus shop to get some antibac gel and wipes as Christ only knows the last time my new office was used/cleaned… This comes to £2.65, which is pretty cheap for the campus shop standards. I neck the rest of yesterday’s breakfast smoothie (I know, I know…this really is not a sufficient breakfast…) and start to prep for today’s teaching.

5pm: What. A. Day. Back-to-back teaching from 11am-5pm! I ate my lunch literally in front of a computer, I didn’t even have time to get back to my office. Really weird because we can’t speak directly to the students during workshops. Usually we would be able to go right up to them and look over their shoulders at their screens (they’re doing stats, so often need technical help). Of course, with COVID restrictions, we can no longer do this. Instead, even though we are physically near them, they have to call us through MS Teams in order to share screens so we can give them direct help. Weird! Nevertheless, it is so lovely to see students and support them.

5.40pm: Sat on the train listening to The Adventures of Huckleberry Finn and A requests £10.21 on Monzo. I wonder wtf he’s bought…

6.30pm: I am home and he is immediately forgiven: gin and loads of toppings for jacket potatoes tonight. Nice one, A, you’re sexy and smart. We tuck into jacket potatoes, such a simple dinner, but so satisfying. We watch Below Deck while we eat.

7.15pm: Have a gin, because fuck it, and read Why Women Are Blamed for Everything by Dr Jessica Taylor while A plays video games. It’s not an uplifting read but definitely very important and I would strongly recommend it to both women and men. I’ve already instructed A that he shall be reading it after me.

9pm: Start watching Dark but I’m too tired to mentally deal with all the conceptual hullabaloo. Instead we get ready for bed. You know me: brush teeth, skincare routine (retinol this time), with the addition of my rose quartz gua sha. We scroll through Netflix for something easy and start watching Ackley Bridge. A and I have both previously worked in challenging education settings, so we immediately really enjoy it.

10pm: A makes us lemon, ginger and manuka honey herbal teas before bed. I put on my sleep mask, do 15 minutes of mindfulness via my Headspace app (currently doing a great course on kindness) and then fall asleep listening to The Murder at Troyte’s Hill by Catherine Louisa Pirkis on The Classic Tales Podcast.

Total: £30.06

7am: A drags me out of bed to go for a morning walk. It’s so lovely once I am actually out of the house. We love seeing all the wildlife early in the morning. Remember, I live in London, so wildlife is defined as squirrels, ducks, swans, runners and people fishing in grimbo Thames water. There are two swans that swim together every morning and it is so romantic. Cutie swans, we love you.

8am: Back from our walk. Showered, brush teeth and do morning skincare routine. Decide to have a no-makeup day today and PRAY TO GOD THAT NO ONE SCHEDULES A SURPRISE MEETING PLEASE GOD. Our Sainsbury’s delivery arrives later – thank the lord. For now I have jam on toast, a smoothie (orange, carrots, banana, turmeric and ice), feroglobin water and an espresso. I also catch up on Money Diaries.

12pm: Had a productive morning! I have been working on the same paper edits as earlier in the week and I am also working on edits for another paper, which I hope to submit for publication soon (fingers crossed). Cheese and ham toastie for lunch, oh yeah. Pair this with Squares and a Curly Wurly (obvs). We munch on this while watching Jack Whitehall’s Travels with my Father, which just cracks us up. His dad reminds me so much of mine.

1pm: Some books I ordered last week have arrived! I bought The Luminaries by Eleanor Catton, State of Wonder by Ann Patchett and One Hundred Years of Solitude by Gabriel García Márquez. I ordered them from Hive, it’s a bit like Amazon but only sells books and they’re all sourced from independent bookstores, plus something like 20% of their profit is invested in these stores. Especially with how bookstores have been impacted by COVID, I like this ethos. I am doing another reading challenge called The Origins Challenge: you write down five countries you’ve never been to and would like to visit and then select a book set in each country and read it. This is all part of a Bookopoly savings scheme I’ve started by bookmoodreviews.com. I am really enjoying the scheme so far and am saving money in a fun way! I would recommend 🙂

1.15pm: My brother, G, rings me for a chat. He works in security at a university and it sounds like freshers has been absolutely hellish. On a brighter note, he and his girlfriend are coming to ours for Halloween and we can’t wait! We discuss outfit ideas. Disclosure: A and I are planning on going as Joe Exotic and Carole Baskin.

2.45pm: Our Sainsbury’s delivery is billed and will arrive between 4-5pm. It comes to £62, which I split with A: £31 each. This consists of: puff pastry, goat’s cheese, mushrooms, eggs, yoghurt, ham, chocolate bars, Belvita, vinegar, coffee, peas, cleaning wipes, butter, cheese, oyster sauce, mirin, rice vinegar, udon noodles, gyoza, cavolo nero, chicken fillets, chicken kievs, onions, wine, borlotti beans, crème fraîche.

4pm: Groceries arrive! Woohoo. Also, a tweed pinafore dress I ordered off Depop arrives and it looks cute af. I am very pleased! Finish working. I have nearly finished the edits on this paper, I just have a few more thoughts which I require feedback on from my supervisor, so I send her an email. Happy to sign off for the day.

4.15pm: Decorators go – see ya! Manage to move things back around in our lounge, which is SUCH a relief. I do a 30-minute abs and booty workout via a MadFit video on YouTube followed by 20 minutes of Yoga with Adriene. GAINS GAINS GAINS. I would normally work out and do yoga a LOT more frequently but I need to work out a new routine now that I am commuting three times a week.

5.30pm: Omg I am dead. I feel like a combination of Morticia Addams and Kayla Itsines: very dead but very pumped. I down some water and start making dinner, which tonight is yaki udon and veg gyoza. YUM. We try to eat vegan/veggie at least three times a week to do our bit for the planet.

5.45pm: A is still working so I let dinner prep rest and run a bath. I soak while enjoying a glass of fake wine and listening to Into The Hum on The Truth podcast.

6.30pm: We eat dins while watching Ackley Bridge and then I prep my lunch for tomorrow (same as earlier in the week). I also make a smoothie for tomorrow: apple, banana, spinach and cashew milk. I also scream internally for a while I DON’T WANT TO WAKE UP EARLY WHYYYY. After this minor breakdown, I make a breakfast quiche and pop it into the oven.

7.30pm: Breakfast quiche ready and in the fridge. A plays video games while I start reading A State of Wonder by Ann Patchett. A couple of pages in and it’s already a yes from me.

8pm: A and I snuggle in bed and read our books for a while. He’s such a cutie and I just love snuggling with him.

9pm: A makes us lemon, ginger and manuka honey herbal teas. We brush teeth and I do my skincare routine (azelaic acid tonight). We chat for a while and then I pop on my sleep mask, do 15 minutes of mindfulness and continue listening to last night’s podcast while I slowly snooze…

Total: £31

5.45am: Nooooooooooooooooooooooooo.

5.55am: This is bullshit.

6.50am: Showered, teeth brushed, morning skincare routine complete, minimal makeup – no time for eyeliner flick. Go to put on new pinafore but it needs a hook and eye or the zip comes undone. Fling pinafore aside, find another outfit in chaos of bedroom, neck an espresso, kiss A, where’s my backpack? Get my backpack, out the door, oh FFS my face shield. Go back and get my face shield, leave the house and BREATHE.

7.20am: En le train and sipping my feroglobin water. Thankfully my body is at a reasonable temperature today. Check my slides for teaching today and then listen to The Adventures of Huckleberry Finn. £17.20

7.30am: Yay – I’ve sold a skirt on Depop! I have stuff that I sold last week that I also need to post, so pop this on my mental to-do list. +£7.20

8am: Have a peruse on Depop as I really need a pair of knee-high boots for work. I have liked and saved a ton of different pairs over the past few weeks but haven’t committed to any yet. Suddenly, I find THE PERFECT PAIR. They are River Island, in my size and only £16?!?! Of course I buy them.

9am: In my office and prepping for the day. Receive a notification that my Papergang subscription has come out. £9. I absolutely love this and it is so worthwhile as I go through stationery at a rate. Excited to see what this month’s design is!

12pm: First lab class down. I was impressed with the students, they were so on it and really engaged – love it! Head back to my office to eat my lunch while simultaneously working on my papers. After this, I read up on the slides I am teaching this afternoon.

1.30pm: Started my period. I’m on the POP mini pill and fall into the category of ‘surprise periods’. I really cba to go and buy sanitary towels when I have about 10,000 at home and five pairs of period pants. I do the old-fashioned toilet roll trick and cross my fingers. Why are wombs so inconsiderate? Unbelievable.

4pm: Afternoon labs complete. That group was a lot quieter. Nevertheless they seem to be grasping the material and that’s the main thing. I meet up with my friend, L, who I used to share a desk with. After a lovely catch-up, we head to a plant sale to buy some plants for our (now in separate buildings, cry) desks. I get two with pots for £12. L and I also make plans to do a double date soon.

4.30pm: My womb is aching so much. Toilet paper is holding out though so fair play to that. Realise I got on the slow train by accident and am silently going through a list of swear words.

6pm: Home, make lots of pathetic sounds and show pathetic body language to A. As much of a feminist as I am, I also like a bit of sympathy sometimes. I drink some choccy Nesquik with hazelnut milk as my sugar levels feel shockingly low and sneak two spoonfuls of Lotus spread. A makes dinner: chicken kievs with wedges and mixed veg. Yum. We catch up about our days over dinner.

7pm: All period jokes aside, I have a splitting headache and feel like shite. Take some ibuprofen and snuggle in bed with A. We watch The Hobbit; our absolute go-to things to watch are any of The Lord of the Rings and related films. Apparently I fell asleep around 8pm. No recollection. No regrets.

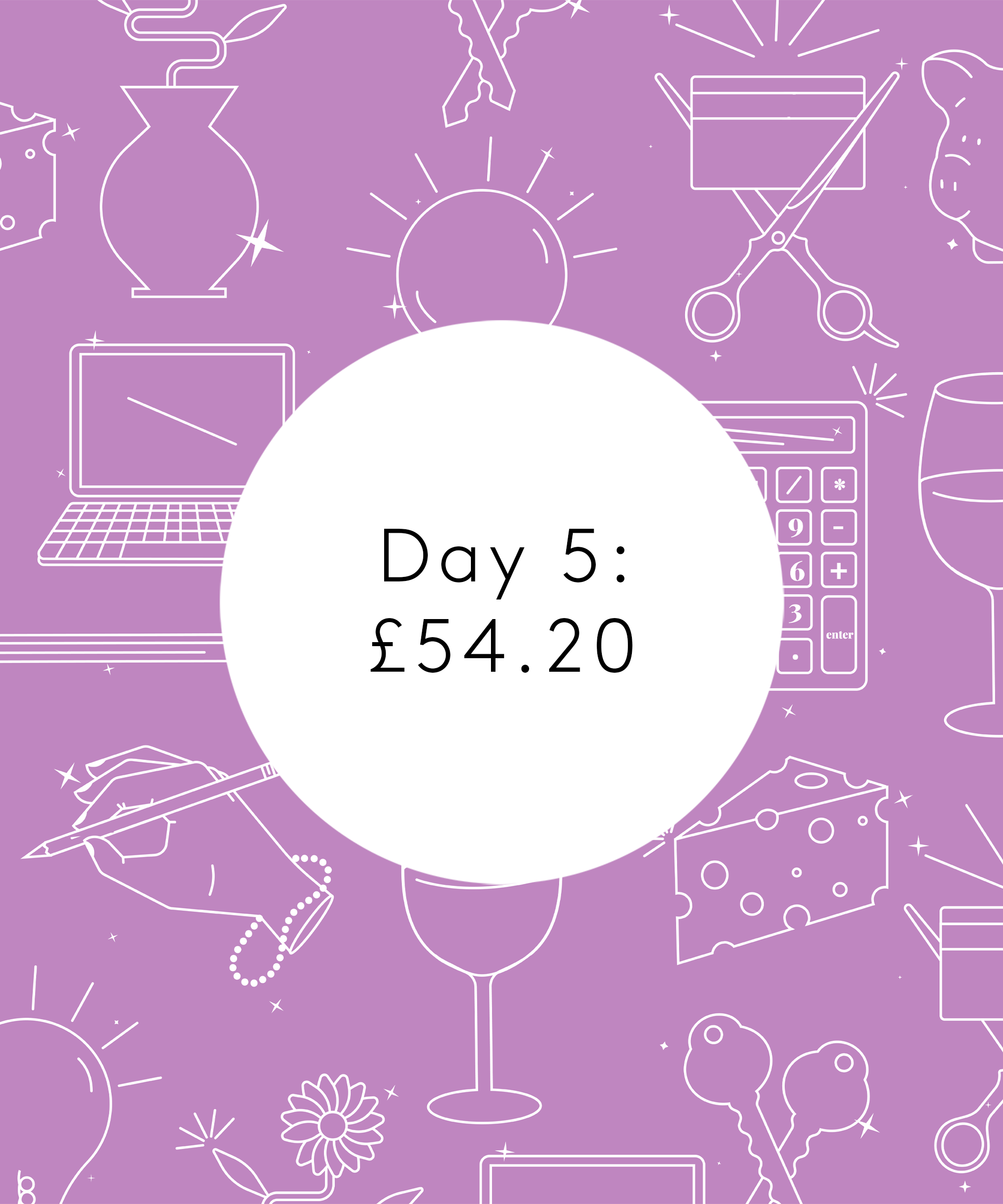

Total: £54.20

5.30am: Did I die? Is this hell?

5.45am: I definitely died. This is definitely hell.

5.50am: Drag myself out of bed and into the shower. Maybe this is how Jesus felt when he rose again? Don’t wash my hair and discover this saves me oodles of time. Just a bit of cheeky dry shampoo and she’s good to go.

6.30am: Shockingly, I am ready with time to spare. A is also coming into work today (lucky bastard only has to teach one day a week). Realise I have not mentioned until now that A and I work/are doing our PhDs at the same uni. We have coffee and breakfast quiche together.

7.20am: Absolutely pissing it down. We manage to get to the Overground and grab first class seats – fancy. I chug my feroglobin water while A and I book next week’s Sainsbury’s shop. £17.20

8.20am: Arrive at work and show A my new office. He is jealous and I love it. Muhahahaha. We pop to the campus shop and I grab some Fanta as my sugar levels still don’t feel tickety boo. I also grab some Lockets as I am doing a lot of teaching today and ain’t nobody got time for a sore throat. £3

11.50am: Jesus lord, I have had such a busy morning already. Firstly, I discovered a stranger in my office who reckoned it was his office? As expected, this resulted in a great deal of emails between admin and myself, and him. He wasn’t outwardly rude but he was very territorial. What is wrong with people? I played the “nice” card but I am plotting his death. Thankfully this works and he goes away. After that fiasco, I cover a lab class for a colleague. It was with first year students, which was really nice as I am eager to ensure that they feel settled and happy despite the COVID madness. Following this, I am back in my office and prepping for two online seminars. Busy, busy!

2pm: Online seminars complete and went surprisingly well with no hiccups. It does feel a bit weird speaking to screens but was nice when students unmuted themselves and contributed. Scoff my dinner (ham and mayo sandwich, Quavers, Curly Wurly) while flicking through Depop. I messaged a seller a while ago, hustling for a bundle of two skirts for £9. She has just responded in agreement – yes!

3pm: Just sold a jumper on Depop. Woop! +£5

5pm: Afternoon seminars complete. School’s out! A meets me at my office and we head to the station while chatting about our days.

8pm: We indulge in a glass of vino while dinner cooks. I’ve made us oven-baked chicken with borlotti beans, cavolo nero and sweet potato wedges. DELISH. We’re watching Ackley Bridge and laughing about how this schools needs an Ofsted ASAP. A pops out to get more wine, hehe. He pays and my share is £6.30.

9pm: Snuggled in bed watching The Hobbit. Apparently I fell asleep around this point.

Total: £35.50

8am: What a glorious lie-in. I feel reborn. Morning snuggles with A and a coffee. This is what all mornings should be.

9am: Up and start getting ready for Dad’s birthday shenanigans. Shower, morning skincare routine, bold makeup (dark red lips because honey, it’s the weekend) and fancy outfit: camel rollneck, leopard-print midi skirt, snakeskin heeled ankle boots, chunky hoop earrings and a 10/10 attitude. Winner.

10am: Hop in the car and praise Jesus that I have half a tank of petrol. Ensure we have all our bits and set off to Mum and Dad’s.

11.30am: Arrive at a balloon shop near Mum and Dad’s. The guy who runs it is an absolute G and I have known him all my life as the balloon man, he’s been selling balloons and party decorations in my hometown for about 30 years. He’s uber chatty and sorts me out with two massive ’70’ balloons in silver, some blue and silver star balloons and some blue and silver confetti. What an absolute babe. £39 for the whole lot and I am IMPRESSED.

11.40am: We pop via Aldi to grab a birthday card, beers and champagne. I bloody wish we had an Aldi near us. £7.90

11.55am: Arrive home and Dad is shut upstairs in his bedroom, lol. We get the dining table prepped with all of his decorations and tend two extremely overexcited doggies. I then go upstairs and lead Dad downstairs with his eyes shut… SURPRISE OLD MAN! Hahaha, he absolutely loves it all. I tell him that we are going for a posh lunch out and he is so excited. Aww, he deserves the world, my dad. Love him so much.

1pm: Arrive at the restaurant and, as requested, a bottle of champers is waiting for us on ice. We have pork crackling and sourdough toast for nibbles, followed by starters (I have a salmon terrine with capers and caraway toast), followed by mains (I have veal sirloin with seasonal veg, parsnip crisps and red wine jus) and coffees to finish. The food is absolutely to die for. The service is also exceptional and we give them a tip. Such a lovely couple of hours eating, drinking and chatting away. I feel extremely lucky to have parents that are also my best friends. They really are the best. A pays and we split it as a birthday treat to Dad and also a treat for Mum. £96.61 my share and worth every single penny.

3.30pm: Back home and feeling satisfied. Mum and I take the dogs out for a spin and then we all chill on the sofas, drinking champagne and having a good chat.

4pm: Just sold an old light mask and a jumper on Depop – sweet! +£10

6pm: Mum serves up cheese and crackers as well as sweeties while Dad picks a film to watch. He decides on Once Upon A Time in Hollywood, which received bad reviews but we all think is fab! I feel so sad for Sharon Tate, she had such a horrible death, but I really like the fact that Tarantino immortalises her in this film and presents her for all of her lovely features rather than just focusing on her death, which is what so many other filmmakers do. We continue drinking champers and snuggle down to watch the film.

10pm: Film finished and we all head to bed after a lovely day. I am really pleased my dad has had a special day 🙂 Snuggle down with A and soon fall fast asleep.

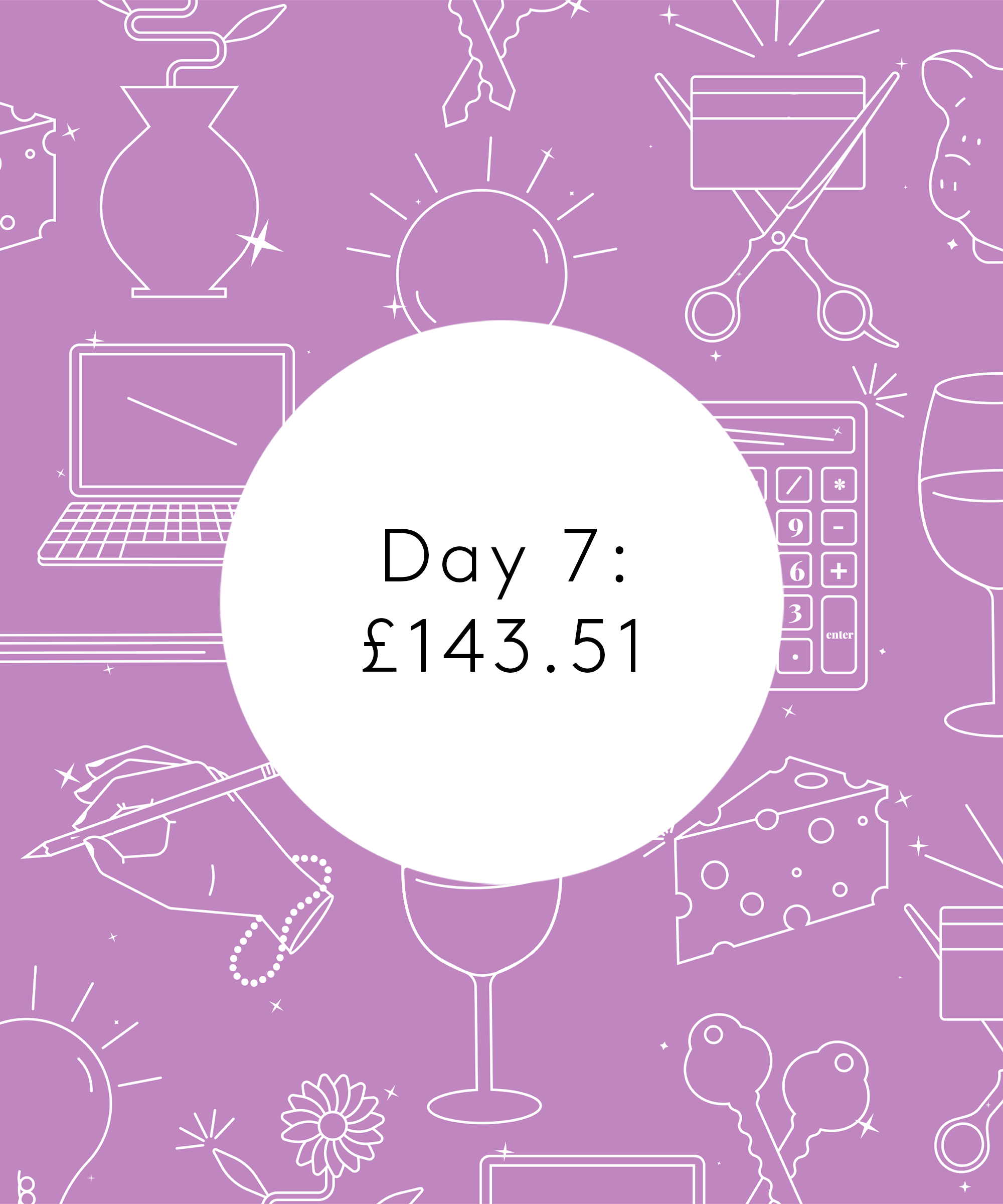

Total: £143.51

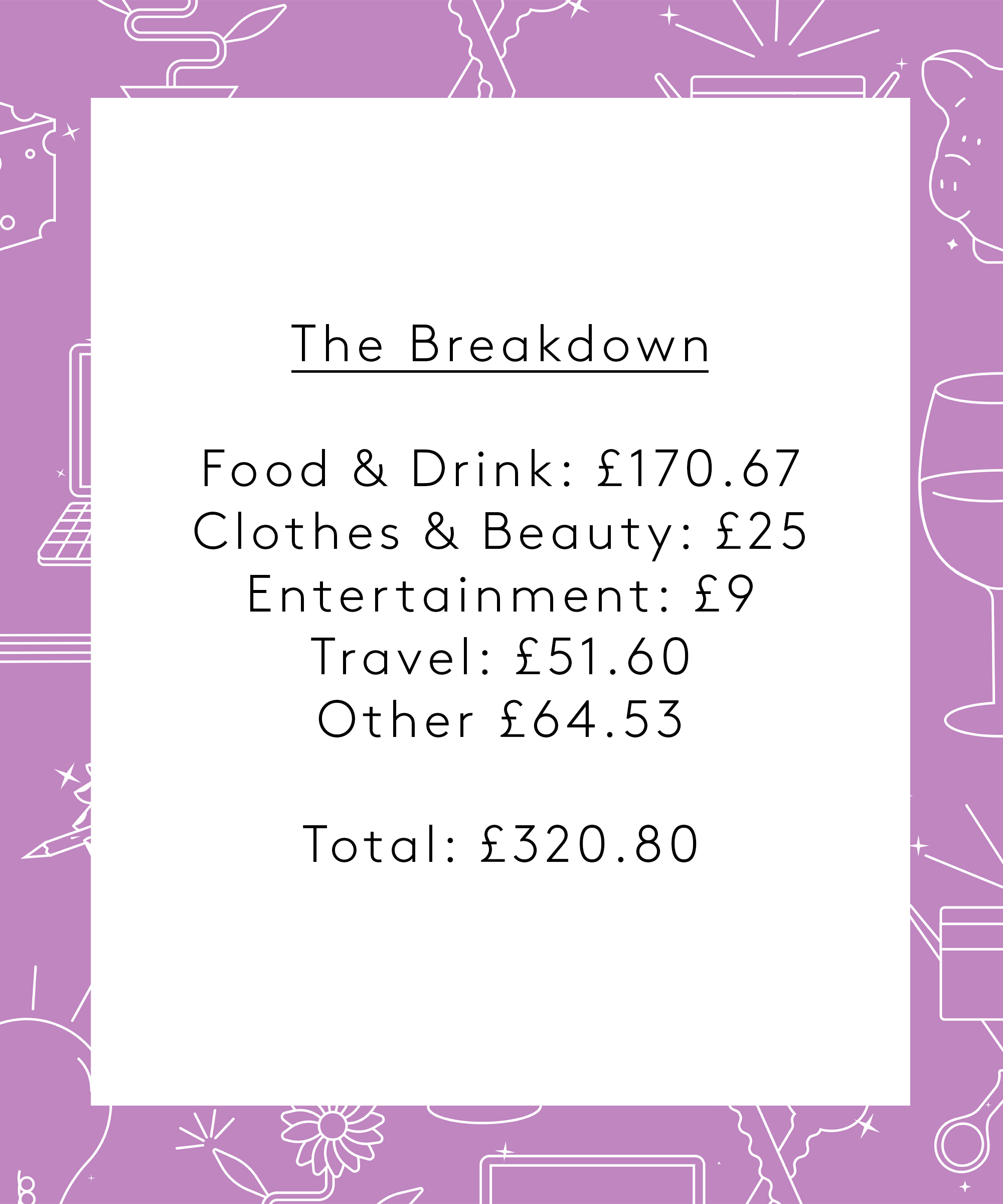

Food & Drink: £170.67

Clothes & Beauty: £25

Entertainment: £9

Travel: £51.60

Other £64.53

Total: £320.80

Conclusion

“I would say that this has been a pretty typical spending week for me, with the exception of buying a few clothes on Depop. I think, overall, I have a good attitude towards money and I’m really not too much of a spender. I would rather spend money on nice meals and experiences rather than expensive items (don’t even dare mention my Chanel handbag fund, thank you very much). I also think I have a rather creative attitude towards saving, such as my Bookopoly savings scheme! I think making saving fun detracts from it feeling like a burden, which can only be a good thing. My savings goal moving forward is definitely to put more money aside for long-term goals, such as adding to my Help to Buy ISA and Premium Bonds. I also want to start putting money aside as I would like to provide my parents with private healthcare in their old age.”

Like what you see? How about some more R29 goodness, right here?

Money Diary: An Unemployed 29-Year-Old In Glasgow